Climate change and the macroeconomy: Implications for the conduct of monetary policy and the coordination of monetary, prudential and fiscal policy

Climate change and the macroeconomy: Implications for the conduct of monetary policy and the coordination of monetary, prudential and fiscal policy

The impact of climate change on the conduct of monetary policy, as well as the contribution of monetary policy to the achievement of the Paris Agreement and the Sustainable Development Goals, are priorities in the NGFS research agenda. With this fourth call for research proposals, INSPIRE aimed to support and complement NGFS research in these areas.

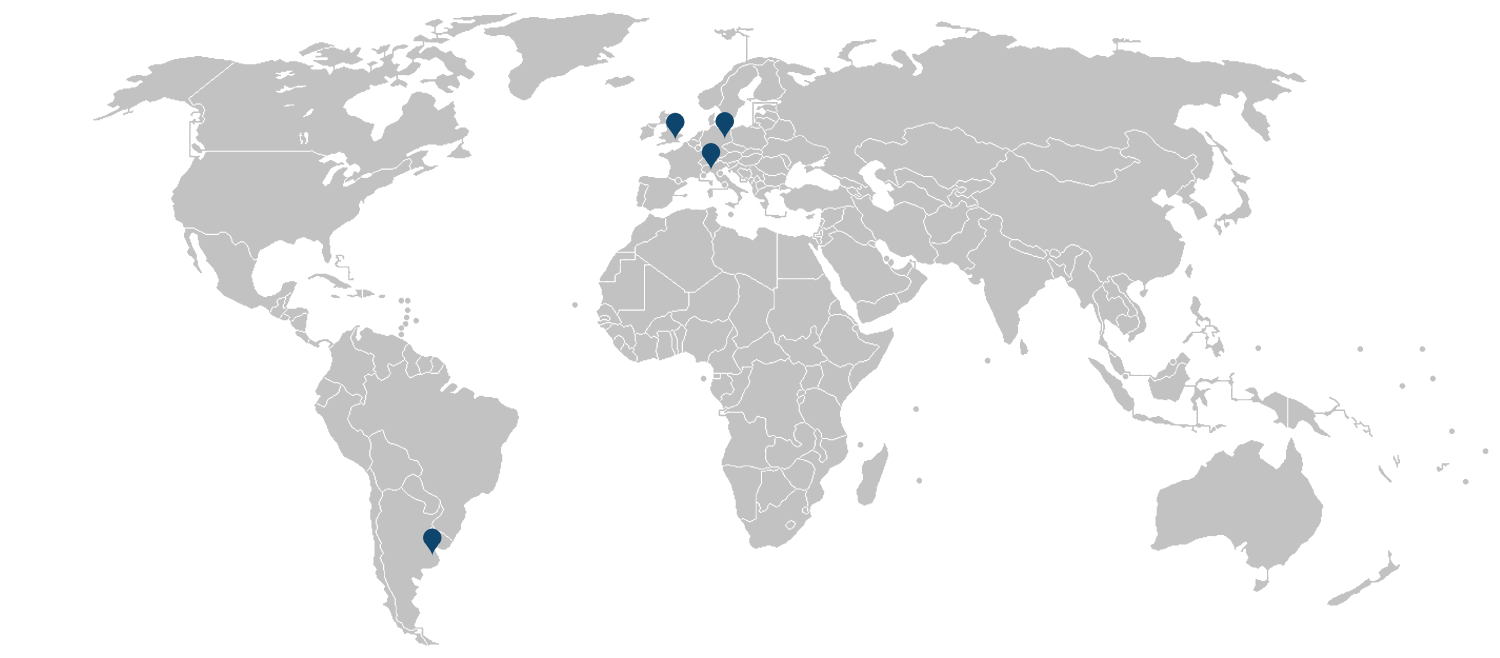

Released in October 2020, we received 33 proposals from teams across the globe. We commissioned four projects conductucted by 16 researchers affiliated with 11 institutions.

Researcher locations

Downloads

Funded projects:

Optimal Climate Change Mitigation through Green Quantitative Easing and Fiscal Policy

We address the question of how green quantitative easing could complement governments’ toolkit for climate change mitigation. In our setup, green quantitative easing refers to a given outstanding stock of bonds held by the European Central Bank and its portfolio allocation between a clean and dirty sector of production. Our key research question is how the central bank can contribute to an optimal inter-generational sharing of the burden of climate change policies in comparison to, or in combination with, fiscal mitigation policies.

We develop a quantitative overlapping generations model in which households consume and allocate their savings and their work efforts between a clean and dirty production sector. A reallocation of the central bank portfolio toward the clean sector increases the capital stock employed for production in that sector relative to the capital stock in the dirty sector. This triggers a relative increase of labour demand in the clean sector and a relative expansion of output. Through this mechanism, the central bank can thus influence relative production across the two sectors in the economy. We then contrast this policy with fiscal policy measures to mitigate climate change. We will explore whether the central bank can improve the economic allocation beyond what is thus achieved through fiscal policy.

Holding constant the balance sheet of the central bank enables us to focus on the portfolio reallocation mechanism. However, it limits the interaction between fiscal and monetary policy in the model. As a next step, we extend the model by an explicit notion of money and the introduction of a distortion that requires bond purchases by the central bank, which will enable us to study the effects of an expansion of central bank bond holdings and of climate policy interactions.

Show Less

Building a macro-financial integrated-assessment model for ordered transitions and fiscal-monetary policy interactions

Assessing the impacts of climate change-related physical and transition risks on the financial system and the macroeconomy is one of the most urgent and prominent needs to support climate policy design. However, the modelling toolbox for the assessment of these risks is currently rather scant.

We contribute to filling this gap by developing a macro-financial model that brings a detailed energy sector into a macroeconomic agent-based model with heterogenous banks and cross-sectoral exposures. The advantage of the proposed framework is twofold: It builds on two consolidated models in their respective domains (macro-financial and integrated assessment modelling) and includes a representation of both micro-level indicators of economic activity (e.g., insolvency rates, mark-ups, productivity dispersion, non-performing loans) and macro-level indicators (e.g., output growth, volatility, unemployment, public debt). Crucially, the macroeconomic properties will emerge indirectly from the decentralised interactions of individual agents and will possibly show non-linear and threshold effects (e.g., due to contagion).

After calibrating the model, we structure the project around two main applications. First, the model will be used to assess how the transition pathways of major emission/socio-economic scenarios and the associated changes in the climate would affect macroeconomic fundamentals and financial stability. Our results will add a macro-financial perspective to the scenario narratives. Second, building on previous work of the project team, we are testing a variety of climate-related fiscal, monetary, and macroprudential policies, with the aim of studying whether a target to physical or transition risks from climate change could hide trade-offs or double-dividends.

Show Less

From Covid-19 to climate change and nature loss: how can a precautionary financial policy framework coordinate monetary, prudential and fiscal policies to address long term challenges?

In the face of climate-related financial risks, the Bank of International Settlements in its ‘Green Swan’ book demonstrated the importance of coordination between green fiscal policy, prudential regulation, and monetary policy. Such coordination must be underpinned by a shift in intellectual framework to facilitate financial policymaking under unprecedented global threat situations.

Aligned with this assessment, we propose to develop the Precautionary Financial Policy (PFP) framework, to address the dual issues of policy coordination and the need for an underlying paradigm shift. The PFP framework provides the theoretical justification for more ambitious financial policy interventions, in the face of the radical uncertainty characterizing long-term and potentially irreversible risks such as those posed by climate change and massive biodiversity loss.

The project will develop the PFP framework as a new paradigm that could support greater coordination between monetary, prudential, industrial, and fiscal policies (henceforth financial-fiscal) in the face of emerging climate- and nature-related financial risks. In particular, we will examine:

- How this approach may provide a more coherent alternative than the ‘market neutrality’ principle in facilitating such coordination, in light of the recent European Central Bank’s declarations questioning this principle, and

- How the PFP could help to deal with the problem of differing time horizons across policy spheres, institutions, and mandates that also mitigates against policy coordination.

The research will involve analysis of historical examples since the 1930s up to and including the most recent policy responses of financial-fiscal policy coordination and expanded institutional purpose to address Covid-19. We will develop a typology of financial-fiscal policy coordination and use this to formulate concrete policy recommendations in terms of institutional setup and governance.

Show Less

The impact of climate change and policies on the balance of payments and central banking in commodity-exporting developing countries

We assess the implications of climate change and policies for monetary policy mediated through their impact on the balance of payments. We examine transitional and physical risks in developing countries where the influence of balance of payments on monetary policy is shaped by the countries’ strong dependence on primary commodities, on top of their larger vulnerability to external financial shocks in comparison with developed economies.

We use two case studies of middle-income countries to conduct this research. We analyse the experience of Nigeria, an oil-dependent commodity exporter, during three sharp declines of international oil prices (the global financial crisis of 2008, the fall in oil prices in 2014, and the fall in 2020 due to the C-19 pandemic). This will serve as an example of the potential impact of transitional risks such as decarbonisation policies and divestment strategies. Regarding physical risks, we take the case of Argentina, a country with a significant share of agricultural products in its export basket. The country is experiencing more frequent and prolonged droughts and floods in main agricultural regions.

The study conducts a mixed methodology approach. The focus will be on export performance, exchange rate volatility, and the implications for monetary policy design and implementation, capturing direct (trade balance) and indirect effects (exchange rate and financial stability) of developments in commodity exports and prices. Immediate effects are assessed with the help of event studies and time series econometric analyses. These quantitative results are triangulated with qualitative data derived from semi-structured expert interviews with central bankers.

Show Less